This is the third in my annual posts about my ISA (tax-free) portfolio. I’ve written before about how there is an outside (~10%) chance of my ISA portfolio reaching $100m, if I live for another 40+ years. Yet, as of my last post a year ago, the total FvL ISA pot was worth ‘only’ £355k (~$500k, back then!). So how am I feeling about multiplying my ISA 200x?

My $100m assessment was based on a scenario analysis over the next 40+ years. Making various assumptions (no withdrawals, regulation changes, etc), if I maintain contributions at £20k x2 per year, and achieve an ‘Above Average Risk’ level of return (>9% per year average, quite a high level of volatility), then in about 10% of predicted outcomes my total pot would reach $100m.

There are a couple of simple mental tricks that help me get my head around this growth. First of all, contributing £20k x 2 per year is quite a lot of money; over 30 years this is £1.2m. To make it easier to think about the growth of this annually-topped-up portfolio, let’s simplistically assume it isn’t annual top ups, but instead is a lump sum of £600k ($750k) in year 14.

Secondly, remember the rule of 70. Assuming I average returns of 7% then my portfolio doubles in 70/7=10 years. At an average return of 10% it takes about 7 years to double. So if I start with $0.5m, and averaged 10% return, after 35 years I have doubled 5 times, and I’m at $16m. But if I add (see previous paragraph) $750k in year 14, this $750k then doubles three times; this adds a further $6m. The two together get me to $22m in 35 years. Now assume I last a further 14 years , which takes me to the average life expectancy for UK males of my age, and I double my combined $22m pot 2 more times. $88m. Not quite $100m, but not far off.

Before you say that 10% per year is unrealistic, I am citing everything here in nominal ‘money of the day’ figures. This is before allowing for inflation. Historic returns for a diversified portfolio can easily achieve 5% per year on top of inflation. This works out as 7-8% per year in nominal figures. 10% is high, I will accept, but not absurdly so. If you have significant fees then you can forget it, but if you hold low-cost passive trackers this is not that unusual.

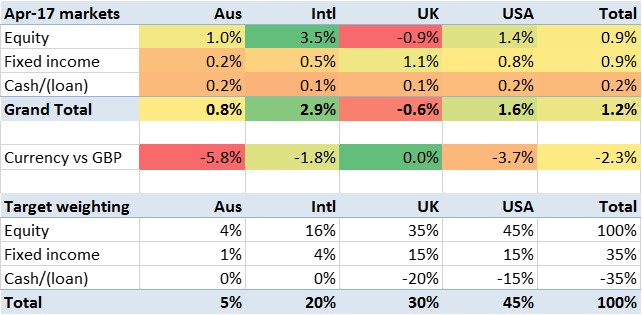

In the meantime, there I was a year ago with £355k. At today’s exchange rate this is barely $450k. How have I fared since then?

Continue reading “How to become an ISA millionaire” →