A year ago I was scrabbling for funds to buy a house, the market was down about 5 points in a month, and Brexit seemed like a tail risk. What a difference a year makes.

My investment portfolio finished 2016 up 24%. A record year. Am I a genius? Was I lucky? Was this normal for stock market investors?

I will wager that most investors, even the sophisticated risk-friendly readers of this blog, returned less than 20% annual gain last year. Feel free to let me know your returns in the comments below as I’d be delighted to hear there are hundreds of similar ‘achievements’ out there but somehow I doubt it (1).

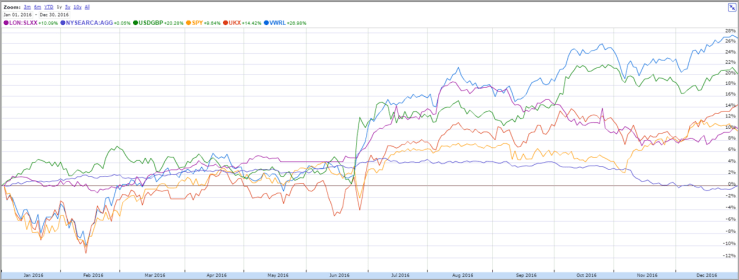

What’s been going on? Well FTSE-100 reached a record high. It’s the red line (‘UKX’) in my graph below. It was in fact up about 14% on the year, plus dividends. So a purely UK equity investor should have been well into double digits.

Bonds had an amazing year too. Despite entering 2016 at ‘unsustainably high levels’, they carried on climbing. At one point in August UK corporate bonds (purple, SLXX) were up 18% in the year. They finished up about 10%. Very few investors would be purely fixed income let alone purely corporate bonds. But a balanced portfolio of, say, 60% equity 40% bonds would have returned about 13%.

If your portfolio returned less than 13% then you have materially underperformed. Which is quite a statement.

Of course as my readers will know I invest much more widely than just the UK. The UK accounts for about 6% of the world’s stock market. The USA is about 50% of it. How has the USA done? Well its bonds (purple, AGG, in the graph below) have not moved in the year, unlike the UK’s (actually they did move *in* the year but they ended up where they started).