The UK’s tax-free savings accounts (ISAs) operate on an annual cycle. Each tax year, starting 6 April, a UK tax payer gets another £20k annual allowance. ISAs are the tax wrappers that administer this allowance. Any account in an ISA wrapper sees all its gains and income become tax free – not even disclosable on a tax return. You can put most type of investment into ISA accounts, certainly including UK/US/EU listed securities. That makes a “stocks & shares” ISA account the number one fundamental of UK taxpayers’ investing, aside from (in some cases) a pension.

£20k might not sound like that much, but if you have £20k to play with as a 20 year old, and you invest it in equities under an ISA, and always reinvest returns, you can expect your investment to appreciate very significantly. At 7% average return it will double every ten years. So by the age of 60, four doubles later, that original sum would be worth £320k (before taking into account inflation). Now imagine that at age 21 you have a fresh £20k to play with. And at age 22. And so on.

I only realised how imperative ISAs were about 15 years ago. But since then I have made topping up my ISA accounts for both myself and Mrs FvL an annual imperative. I try to do this as early in the tax year as I can – in fact I usually start hoarding cash a few months before the start of the tax year in April. And I typically publish a blog post when I achieve it. This tax year, this is that blog post. It has taken me until December to scrape up the £40k readies.

We ended November in the UK with the same prime minister that we started with. That makes a change on October and September. Moreover, our chancellor of the exchequer (Finance Minister, in any other country!) remained in place too. A sigh of relief at these green shoots of stability could be felt all over the place – not least the political podcasts and Op Ed columns.

The UK government released its well signposted ‘Autumn Statement’, having successfully previewed almost every key measure in it. Bankers bonuses remain uncapped, but almost all the other moves from Truss/Kwarteng have been reversed. Notional tax rates are unchanged, but thresholds are either fixed or have been reduced, so there is a bit more tax to pay all round.

The main changes for me are the drop in the 45% tax threshold by £25k, and the corporation tax staying ‘high’ at 25%. The reduced 45% tax threshold adds 5% x £25k i.e. £1250 of tax to my annual tax bill, and corporation tax being 6% higher than it might have been will cost me considerably more than that.

Input prices are falling

Meanwhile, elsewhere in the markets there was a distinct sound of air coming out of the inflation balloon. Some key input prices have dropped significantly in recent weeks:

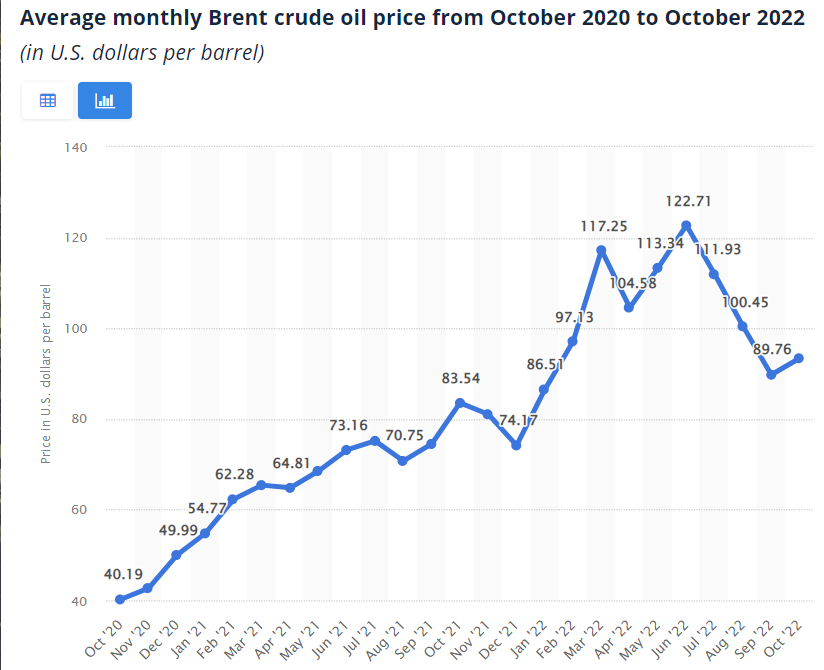

Oil prices are down below pre-Ukraine levels, and about 25% down from peak.

Here in the UK, many have taken pride in our enlightened energy policies.

We led the world, under Mrs Thatcher in the 1980s, with privatising state utilities – so our gas, electricity, telecoms etc are all in the hands of private companies. Guarding against the natural tendency to monopolies in such sectors are our industry-specific regulators OFCOM and OFGEM.

Not for us the Japanese/German greenery-gone-amok policies of turning off nuclear power mid life. Not for us the hypocritical and myopic German policies of reliance on brown coal and Russian monopoly gas. And not for us using fracking to unleash new reserves under our precious, fragile, green and pleasant land; we’d rather let the Americans do this in their flyover states and then pay them, now a net energy exporter themselves, a premium to liquify it and send it over to us. Who wouldn’t?

And to top it all, the UK has been one of the fastest markets to adopt Electric Vehicles (EVs), hastened by a variety of subsidies and tax incentives. EVs pay lower car taxes, lower congestion taxes, lower parking fees, and could be purchased with the help of several thousand pounds of subsidy. Over half of new car enquiries are for EVs, and over 20% of new registrations are for pure or hybrid EVs.

Being in the vanguard in 2019

The results of these enlightened energy strategies have seen our CO2 emissions fall faster than most OECD countries. We were paying, until recently, only a modest premium for our greenification. Consumers have had a choice of over 70 companies, and many hundreds of tariffs – allowing such innovations as Electric Vehicle-specific tariffs, empty-property-specific tariffs and tariffs accumulating loyalty points. And our privatised, competitive model has been ‘improved’ with a Labour Tory retail price cap, restraining operators from milking the can’t-be-bothered-to-shop-around segment.

The chart below shows what this felt like chez FirevLondon back in 2019. Those halcyon days when I worked away from home five days each week, drove a petrol car, and lived in one house – admittedly my Dream Home. The Dream Home consumed around 46k kWh of energy each year – admittedly far more than an average (smaller) UK household – yet cost me less than £250pcm of energy. My car usage was far less than an average household, so the fuel for that cost me only around £1k per year – ensuring I could drive a large-engined funmobile ‘cheaply’ (25p/mile doesn’t add up to much if you don’t drive many miles!). My total fuel costs amounted to less than £4k per year. Of that, the taxman received around £840 p.a. of tax and fuel duties – chiefly from my petrol car. Energy is taxed at a reduced rate of Value Added Tax (VAT) of 5%, compared to 20% for normal expenditure.

Energy costs p.a. in 2019

How times change

Now, unfortunately, in 2022 it turns out that the world looks completely different.