March took ages. Heck, there was even a blue moon. So much seemed to go wrong I am probably going to miss stuff out.

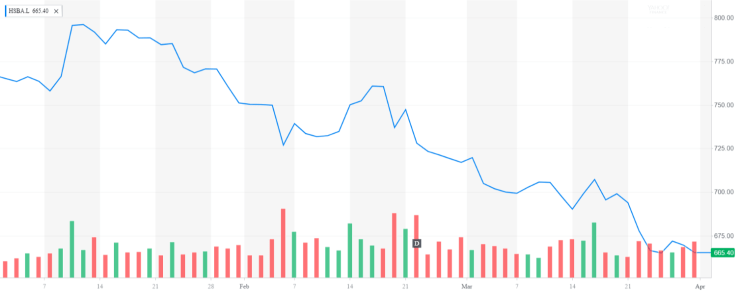

Obviously Trump started a trade war. I’m not sure the exact impact on the markets but I think this marked a clear Sell signal for S&P500. I often think of HSBC as a proxy for global (esp. Asian) trade, and its stock tells the story as well as any. March wasn’t particularly notable except that the miserable Q1 trend continued, with hardly any respite.

Next, and closer to home, Aviva kicked off some unwelcome news by announcing they were going to redeem their irredeemable shares. Or something similar. I own a bunch of similar holdings (notably NWBD and LLPC, after a helpful tip by Monevator back in 2010). Anything which looked like a blue chip pref share with any sort of ‘irredeemable’ tag got clobbered, not entirely surprisingly. I did a handy table mid month showing the extent of the damage inflicted, at peak. At one point I was down almost 1% of my total portfolio thanks to this mess. Talk about unexpected correlations.

Fortunately, by month end Aviva had relented and these holdings had mostly regained their poise. I think hindsight will show that we were lucky it was Aviva which played with redeemable fire here – Aviva has a strong ethical position and was successfully shouted down by small shareholders. Had RBS/Lloyds/Santander had a crack I am not sure we’d have been so lucky. And now it will be harder for anybody else do have a go in the future.

While we are talking about unforced errors, for some reason the global media decided March was the time to take down Facebook 50m pegs or two. Having read Dominic Cumming’s riveting BrexitRef blog post, I somehow felt that this news horse had bolted about 18 months ago, but I must have missed something. In any case Facebook’s market cap shed about $40bn, which is a lot of unicorns.