What a month. First of all we get Theresa May’s Brexit 12 point plan, a.k.a. rebranding Great Britain as Global Britain (despite its lack of resonance with voters). Next we get the Trump inauguration. Then we get Trump’s hyperactive first two weeks. Never mind the hackneyed First 100 days of a new POTUS – Trump has done more damage to the USA’s overseas reputation less than 14 days into the job than Bush / Obama / etc managed in their first year.

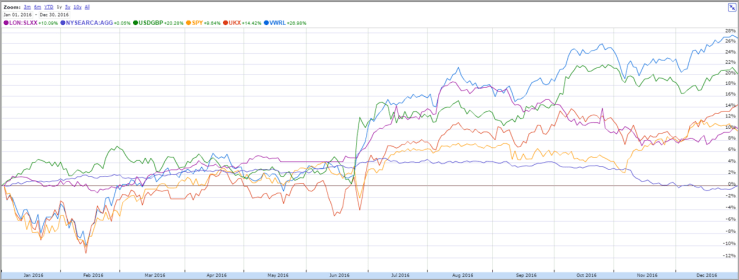

Amidst all this the equity and bond markets have struggled to form a view. USA equities are up a bit, UK bonds are down a bit, not much else to report. Phew.

The USD has fallen a bit, thanks to concerted talking down by Trump and his putative administration. They are accusing China of being a currency manipulator (which appears to be broadly true, albeit in the opposite direction to their claims), Germany of being an EU hegemon and currency abuser (for which there are quite good arguments, so I watch this meme with interest) and Mexico of, well, I’m not even going to go there.

For some reason the AUD has risen against the pound. I’m not sure why. Combined with the USD fall this is quite a big shift in the terms of trade between Australia and the USA.

Continue reading “My performance in Jan ’17 – Trumping begins”