It’s the end of the second quarter. That means it’s time for my usual monthly portfolio performance along with a quarterly review of how 2017 is progressing.

June’s news was dominated by the UK’s general election. To my mind the electorate called it about right. Under the UK’s first-past-the-post constituency system no voters have a say on the overall leadership, but nonetheless the overall outcome often reflects the wider mood of the nation with uncanny fidelity. That’s what seemed to happen here: the Tories were badly led down by their leader, and Corbyn’s Labour offered a genuine and, to many, welcome alternative. Yet at the end of the day the Tories remain in power, with an extremely short leash and an exploding collar.

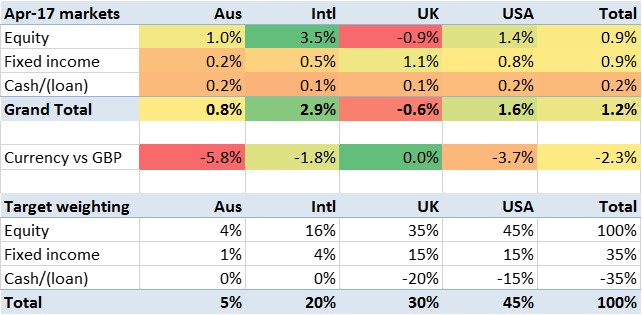

The other news in June, which if you blinked you might have missed it, was the central banks publicly stuttering about the next policy move. This unsettled UK and USA markets noticably, but it seems to have lasted less than a week. From the point of view of my process however this was material; the pound gained about 3% culminating in it reaching $1.32 at exactly the end of the month (see graph). Even as I write this, a few days later, the pound has reverted – but as I took my portfolio snapshot on 30 June my quarter-end numbers were pretty different.

The other news in June, which if you blinked you might have missed it, was the central banks publicly stuttering about the next policy move. This unsettled UK and USA markets noticably, but it seems to have lasted less than a week. From the point of view of my process however this was material; the pound gained about 3% culminating in it reaching $1.32 at exactly the end of the month (see graph). Even as I write this, a few days later, the pound has reverted – but as I took my portfolio snapshot on 30 June my quarter-end numbers were pretty different.

Even a week before the end of June I was having a positive month. But thanks to the pound blipping upwards at the last minute, and most of my portfolio being overseas at this point, I recorded a negative month. If the pound remains at the level it’s already returned to, then I am highly likely to post a positive July.