Of course it’s been the month that the UK’s Prime Minister went to hospital, with a “50:50” chance of making it out alive.

Lockdown has been the word on everybody’s lips. I spent the entire month working (hard! Even a bit over the long Easter weekend) from home. And, while the UK extended its lockdown from 3 weeks to 6, by the end of the month the lockdown mood music from across Europe and beyond had noticeably improved.

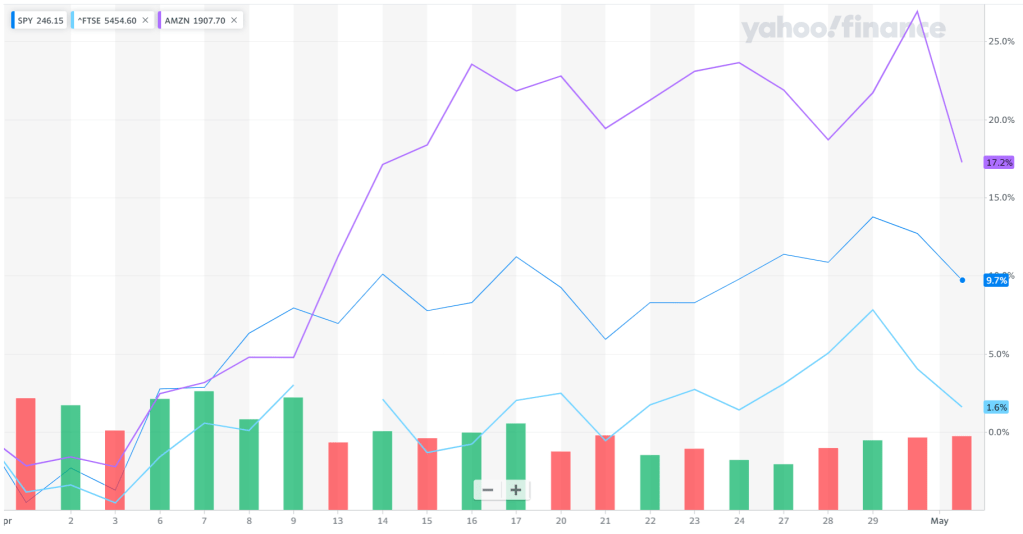

Markets up almost 10%

And, my, how the market’s mood had improved. The US, the S&P rose from 2462 on 1 April to 2923 on 29 April, a rise of 19%. In a month. If you had the courage to burn dry powder on US equities in late March you could have seen over 20% gains since. My (slightly leveraged) “US tech” equity subportfolio rose about 25% – led by Amazon breaking to new highs above $2400.

S&P 500, FTSE-100, AMZN over April

US equities were in fact the standout winner, up 13% in the month, while other equity markets rose 4-6%. In part, this reflects ‘big tech’ (which account for >10% of the US market). Bonds had a pretty good month too, aside from in Oz – where the currency recovered 4%.

What a brutal month. We moved from ‘crumbs, Italy’s borders are shut’ to ‘whoa, we’re all under house arrest’ in only a few days. The start of March is hard to remember.

The Prime Minister demonstrating Covid-19 to us all

I’m glad I managed to get a few days skiing done earlier in the season – now I have three overseas trips cancelled and don’t expect even to leave London for potentially months.

As lockdown loomed, I found myself shocked to be asked “are you staying in London? Or getting away?” by several people. OF COURSE I’M STAYING IN LONDON. In my Dream Home, silly. In fact some friends who had decamped to Cornwall have recently returned to London saying they really hadn’t appreciated how much better to be marooned here than there.

Market meltdown

But turning to the markets, they have had an absolute whipping this month. The fastest decline ever. And, wow, the volatility. Normally liquid ETFs had pronounced spreads, and one of my online brokers resorted to manual trading on a frequent basis. Yet, with all said and done, the damage isn’t yet quite as bad as it feels.

Having caught a cold in February, world markets developed a very nasty flu in March. All equity markets fell. And fell very rapidly. Equities were down around 18%, across the piece.

I am about a week late writing this monthly update, and my what a week it’s been.

February was when the coronavirus (now called covid-19) began to impact the markets. My diary called it the ‘corona correction’. At the time of writing, on the 10th March, the February story already seems rather old, but here it goes in extreme brevity.

Beginning of February. I sold my house, pocketing over £1m cash.

Middle of February: I ‘slowly’ dripfed £1m cash into the market, matching my target allocation.

End of February: the market fell almost 10%. Doh.

(early March – my house money has all gone…. but that’s getting ahead of myself!)

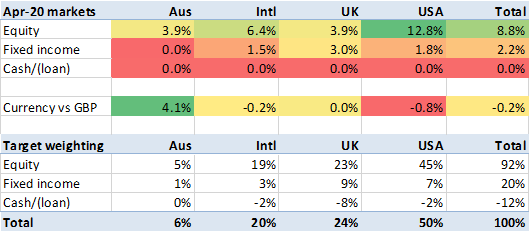

More specifically, equities fell 6-9% on the month (and significantly more off the mid-month peaks). Bonds ticked upwards very slightly. And the pound fell slightly versus other major currencies.

Feb 2020 market & currency movements

The markets, weighted to my allocation, fell 5.8%. My (very slightly leveraged) portfolio fell 6.4%, even more than the market – reflecting me topping it up by >£1m mid month, at its peaks. That high plateau you see in the graph below almost exactly mirrors the time period over which I put my money to work. Sigh.

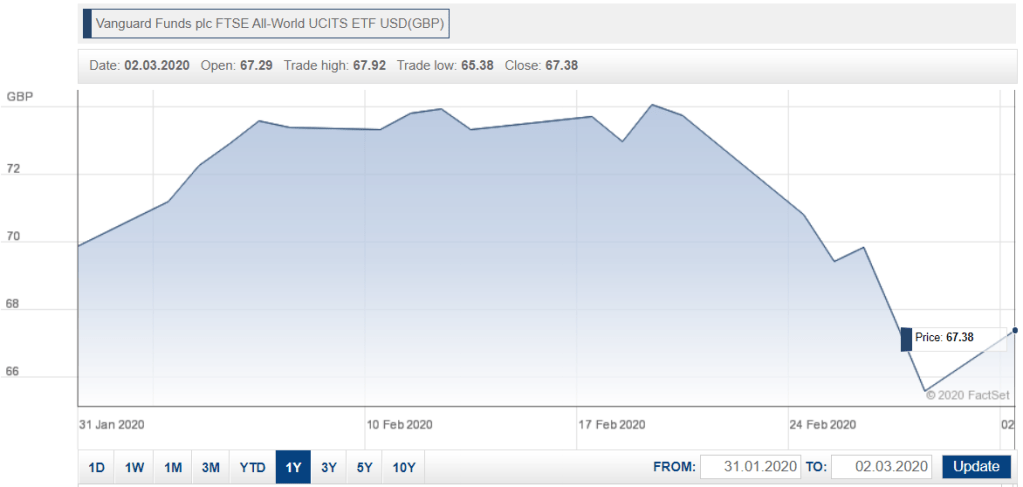

World equity markets – daily movements in February

The other thing February was notable for was my efforts to reduce my (taxable) complexity. I sold a number of holdings, in unsheltered accounts, replacing them with fewer, larger, mostly ETF holdings. And in my sheltered accounts (pension & ISAs), I sold a bunch of ETFs and bought individual securities – concentrating my active holdings in the (undisclosable) tax sheltered accounts, and reducing my number of (disclosable) tax holdings significantly.

My efforts fighting complexity were more successful, more quickly, than I would have first thought. I have reduced my total holdings to <150. My unwrapped (disclosable) holdings are almost below 100 – a reduction of 37 since the start of the year. And my number of small (<£20k) holdings has dropped to 35 (though the market’s falls are making this target harder to hit!).

Progress towards Q1 complexity targets

My portfolio is still complex (certainly too much so for @mathmo – see comment below), but progress is being made – and quickly.

I liked FireVLondon’s revelation on the road to Shipley Tax Office that complexity was a real cost like fees and taxes. I myself just a few weeks ago pinged my tax return off with just 10 lines of information to my accountant so his inventory of tax filing effort was eye-opening. I’d suggest the solution didn’t go nearly far enough in the face of active naughtiness — if the cost of complexity were properly measured, the knife would have cut much deeper.

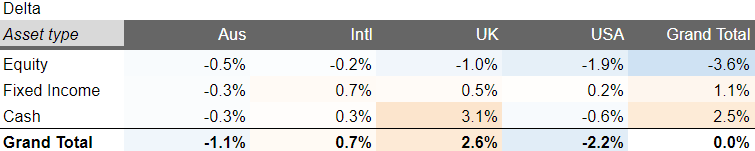

At the end of February, I was almost 4% underweight equities, around 1% overweight in bonds, and 2.5% overweight cash. With hindsight, not terrible positioning for the March roller corona-ster.

Deltas from target allocation, as at 29 February 2020