According to the statistics, most of the readers of my blog are among the highest earning and/or richest people in the UK.

I bet however that not many of you feel that way.

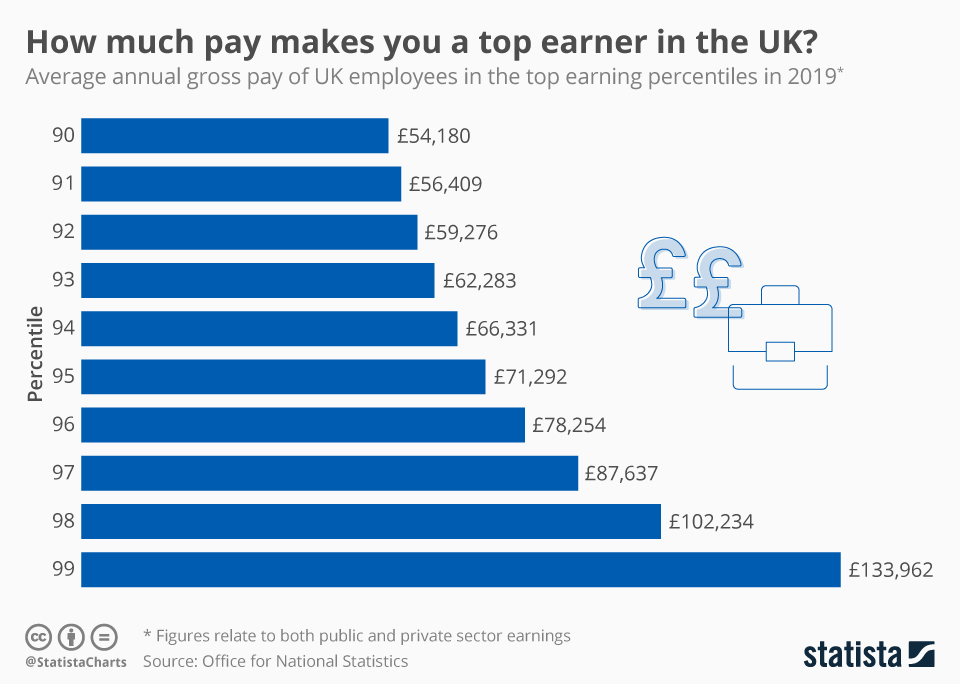

Let’s start with income

To be in the top 1% of earnings in the UK in 2019 required pre-tax earnings of at least £134k. To be in the top 10%, you need to earn (individually) about £54k. By 2023, inflation has probably increased all these numbers by at least 10%, to say £150k and £60k.

Regular readers will know what a fan I have been of margin lending from Interactive Brokers. No longer. If you’ve read my other posts (like this or this or this) on margin lending, and are interested in exploring further, make you read this post before you do.

Why I used to like IB’s margin loans

IB offers credit secured on its portfolios, priced very competitively. This provides remarkable flexibility, at a low price. I have been an eager user, enjoying how I can stay (more than) fully invested but still find funds fast to make an unexpected angel investment, pay for a home improvement project or settle a tax bill. In reverse, I can repay instantly and very flexibly, and I can convert either cash holdings or loans from one currency to another instantaneously.

These advantages apply both to IB’s loans, but also to the portfolio loan I have from my private bank. However IB is much easier to operate, thanks to their excellent online platform and reporting. And IB is cheaper. So IB has been my ‘go to’ lender.

But my net worth includes an important asset class – property – that I don’t normally track, but which I have held in some form for over 20 years.

So, this post takes a look at how my real estate assets have performed.

Real estate works completely differently, for me, than my investment portfolio. For starters, I have never bought a home as an investment. But let’s start at the beginning.

My property owning history

I nearly got on the property ladder in the mid 1990s.

I hadn’t realised, until a friend pointed it out a few years too late for me, that in fact one of the easiest times to get on the property ladder was the moment when I graduated and moved to London. My first job earnt a reasonable London salary of just over £20k, and 1 bed flats in a reasonable part of Zone 1 in London were available for under £70k (now £800k-£1m, sigh).

Mortgage rates had dropped from >13% in 1990 to around 7%. The interest costs could have been around £5k, a quarter of my first-job income. That was in the mid 1990s. It didn’t occur to me to buy a place, and of course those property prices were so high…..

By the late 1990s, buying a property had become a lot harder. But once I was earning £40k+ I decided to take the plunge. I found a reasonable 2 bed place very close to Zone 1 for £200k (now £500k). The mortgage (at around 7% interest, i.e. interest costs were £13k, a third of my gross income) and the deposit (£20k, if I remember rightly, for a 90% mortgage) were a massive stretch….. and then I was gazumped. By the time I reorganised, the places I wanted cost £220k+ and I couldn’t quite afford it.