It’s been a much calmer month in the markets.

Of course it’s been the month that the UK’s Prime Minister went to hospital, with a “50:50” chance of making it out alive.

Lockdown has been the word on everybody’s lips. I spent the entire month working (hard! Even a bit over the long Easter weekend) from home. And, while the UK extended its lockdown from 3 weeks to 6, by the end of the month the lockdown mood music from across Europe and beyond had noticeably improved.

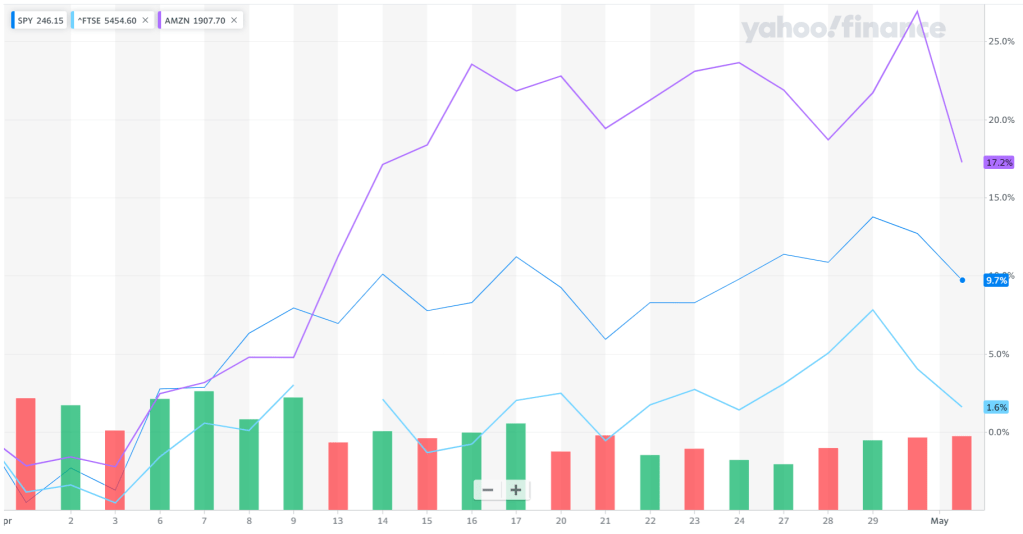

Markets up almost 10%

And, my, how the market’s mood had improved. The US, the S&P rose from 2462 on 1 April to 2923 on 29 April, a rise of 19%. In a month. If you had the courage to burn dry powder on US equities in late March you could have seen over 20% gains since. My (slightly leveraged) “US tech” equity subportfolio rose about 25% – led by Amazon breaking to new highs above $2400.

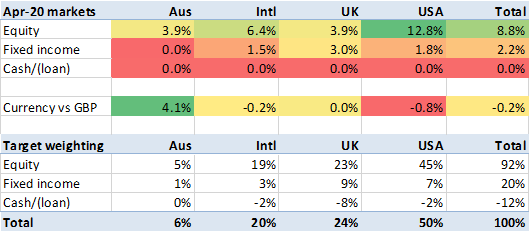

US equities were in fact the standout winner, up 13% in the month, while other equity markets rose 4-6%. In part, this reflects ‘big tech’ (which account for >10% of the US market). Bonds had a pretty good month too, aside from in Oz – where the currency recovered 4%.

What’s going on : is it QE?

I have been finding the market hard to fathom.

Continue reading “April 2020: A mad bounce”