The big news in the UK this week was the latest Budget by the Chancellor Rachel Reeves.

The scare story in the budget runup

All UK readers of this blog will know that the rumours and counter-rumours in the run-up to this budget exceeded anything we have seen before.

There were too many rumours in advance of the budget to catalogue properly here. But I want to highlight several key rumours:

Taxes up by 2%. For a crucial couple of weeks in November, the government was rolling the pitch to break its manifesto pledge by increasing income taxes by 2%.

National insurance on investment income, notably property rental income. This rumour felt credible to me, because it happens elsewhere – such as Ireland. However most of the commentary missed a key characteristic about NI which is that there is an Upper Earnings Limit of around £4k per month (£50k p.a., roughly) above which you only pay 2%, not 8% (or, until quite recently, 12%).

Mansion taxes. The key rumours here were that there would be a tax of 1% on ‘mansions’ above the value of £1.5m or £2m. This move would have been the most impactful for me – with over £8m in two ‘mansions’, I was facing potential £40k p.a. of an entirely new tax.

Pension changes – potentially reducing the ability to take around 25% tax-free, for instance.

And we’re off, into 2025. Before we get too far, it’s time to take stock (pardon the pun) of 2024. I’ll follow the 7 point approach I’ve used for the last few years, starting with the wider market context.

Q1 How did markets do?

December saw falls across most asset classes – arguably reverting to the mean after the November gyrations caused by the Trump election win. The Australian dollar continued its significant fall, with the markets worried about the Trump tariff threat against China – a key export market for Australia.

Equity markets’ performance in 2024 look strikingly similar to that of 2023, with the exception of the UK – which returned almost 10% (including dividends), roughly twice its 2023 result. Equities in the USA rose almost a quarter (2023: 26%), and in other major markets rose around 10% (2023: 10% in International, 12% in Australia, exactly the same as 2024).

Bonds’ performance looks quite different to the 2023 figures. US bonds rose 1%, UK bonds dropped 4% and others were flat, whereas in 2023 Bonds rose 3-5% across all major markets.

And looking at currency movements, the pound continued to climb in 2024 against most currencies, except for the dollar – where its initial climb ended up as a modest fall, with USD up 1.8% against the GBP. The pound now buys over 2 AUD, a striking change from 2 years ago when it bought 1.75.

2024 market returns, by geography and asset class

Using my global weightings, ‘my’ index rose 16% in GBP terms.

The other benchmark I track is VWRL Vanguard’s world equity tracker. With the US now almost 60% of global benchmarks, and S&P up more than double other markets, VWRL rose 18% in 2024.

Q2 How did I do, vs my benchmark?

Portfolio growth

My portfolio rose 16% in 2024. Almost exactly in line with my weighted market benchmark. 16% sounds like a good number versus my long term average of about 9.5% p.a. However in fact, I never actually see exactly 9.5% returns; years deliver either a lot more than that, or a lot less. So 16% is essentially my ‘median’ result; it is the 6th best result out of the last 12 years.

One way to think about my portfolio’s allocation is that my leverage – my portfolio loan – is being used to buy Fixed Income. My loan is about 16% of the portfolio’s value, and my Fixed Income allocation is about 18%. So you could say I have taken out a loan on the Equity house to build an extension, and the extension is Fixed Income.

This isn’t usually how I think about it, because I think I would have some Fixed Income in all weathers, whereas I wouldn’t have c.100% equity exposure if I didn’t have a margin loan. But for the purposes of my mental arithmetic, looking at my portfolio and saying “‘”I have about 20% leverage, which I used to buy assets which fell about 1% in the year, and I pay 6% interest on” is roughly what happened. I.e. my portfolio was negatively impacted by everything that wasn’t equities, including my leverage.

In any case, your actual mileage will vary primarily based on how much exposure you had to US tech, either directly or via S&P500. Any portfolio that was primarily US equities will have done better than mine, and any that had less than 50% exposure to the USA will have been unusual to have achieved 16% gain in the year.

It’s the start of a calendar year. Let’s take a look at what 2023 did to me financially. I’m following the same structure I’ve used for the last few years (2022, 2021, and 2020). Overall, 2023 was a good year on almost all measures – thanks in particular to Q4 which saw the US stock market drag the year into a top quartile performance.

Q1 How did markets do?

First of all, what happened out there? Well, the year felt pretty ‘meh’ for the first nine months – as illustrated by my rather depressed blog post in mid October. But almost as soon as I hit Publish, the US market in particular led a dramatic recovery – reflecting a sharply improved outlook for inflation and interest rates. You can see below firstly the performance in December.

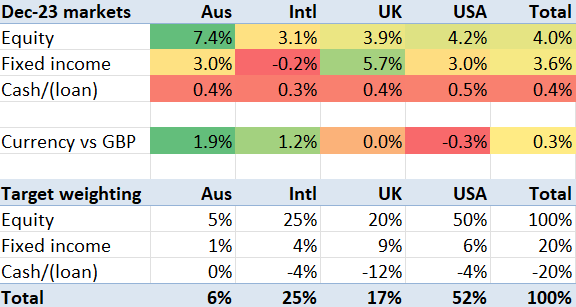

December 2023 market returns, by geography and asset class

Then we get to the year as a whole. Bonds rose by 3-5% across the board, but equities did strikingly better – particularly in the USA where the S&P500 rose around 26%. The UK equity market looks like the runt of the litter, which given the tech-driven nature of the uptick and the lack of UK tech wouldn’t be a big surprise. However it isn’t quite that simple, because the GBP rose against most currencies.

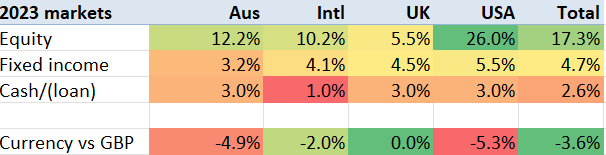

2023 market returns, by geography and asset class

Another way to look at the benchmarks is to look at the world equities (e.g. VWRL) and world bonds (e.g. AGG/BND or the UK’s IGLT). My portfolio has often pretty closely tracked the VWRL ETF. The graph below shows VWRL and IGLT’s share prices (but not dividends) for the year, showing the world equity bundle up (in GBP) 13.4% and the UK government bond index roughly flat.

2023 performance of Vanguard World Equities, and UK Government bonds (excluding dividends)

Q2 How did I do, vs my benchmark?

Against that backdrop – bonds up a bit, equities up considerably more especially in the USA, how did my portfolio perform?