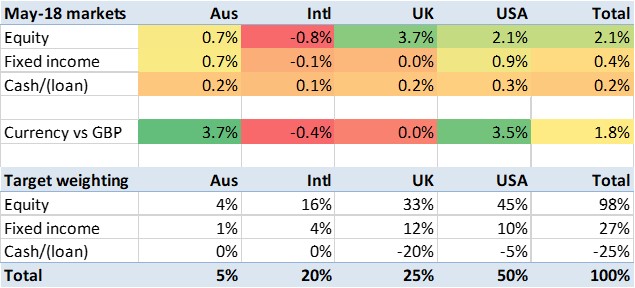

So far as I can see the key geopolitical news in July was a distinct improvement in the US trade war music, if war music is a thing. In particular the EU:USA dynamics improved dramatically when the EU Commission President, Jean-Paul Juncker, showed Trump how to paint trade by numbers.

Given that markets had been fretting that Trump would start punitively taxing German cars, which he has supported for several decades, the Juncker announcement that the EU would buy more soyabeans had a surprisingly positive effect. Or at least, that’s how I account for the 3-5% increase in equity markets in USA/International (Europe), compared to just over 1% in the UK/Australia markets I track.

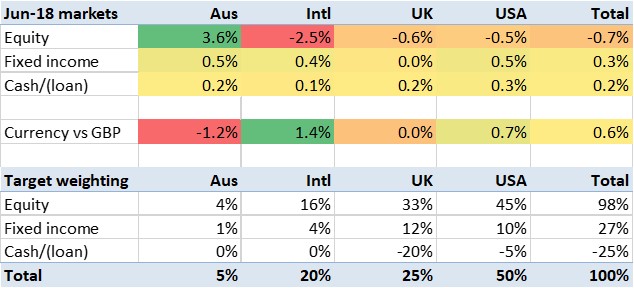

In other news, the pound fell a bit, and correspondingly the UK equity markets rose a bit. I don’t really know why Oz equities were up, in sterling terms, by 2% for the second month running, but I’m certainly not complaining.