I have to take my hat off to Theresa May for her performance in October. Dancing (well, jiving, at least). On stage. To kick off her make-or-break appearance at the Tory conference. That lady has balls.

The big news this month has been foreign. Alien, even, in the case of another lady with balls – Jodie Whittaker (“Why are you calling me Madam?”) breaking the Doctor’s glass ceiling.

We’ve had Saudi Arabia in the news for much of the month, for some gruesome reasons. We’ve had foreign governments getting a whipping in Germany or, Royal visit notwithstanding, losing their majority in Oz. We’ve had the USA administration pulling out of a Russian nuclear arms treaty.

And of course, we’ve had the major geopolitical upheaval that is a new phone from the most important FAANG.

I suppose a quick recap of the worldwide developments would, on balance, suggest downward pressure on the markets.

I really don’t think however that Doctor Who, returning to Earth after a prolonged absence and reviewing recent developments, would expect such a brutal, consistent month in the equity markets. Everywhere.

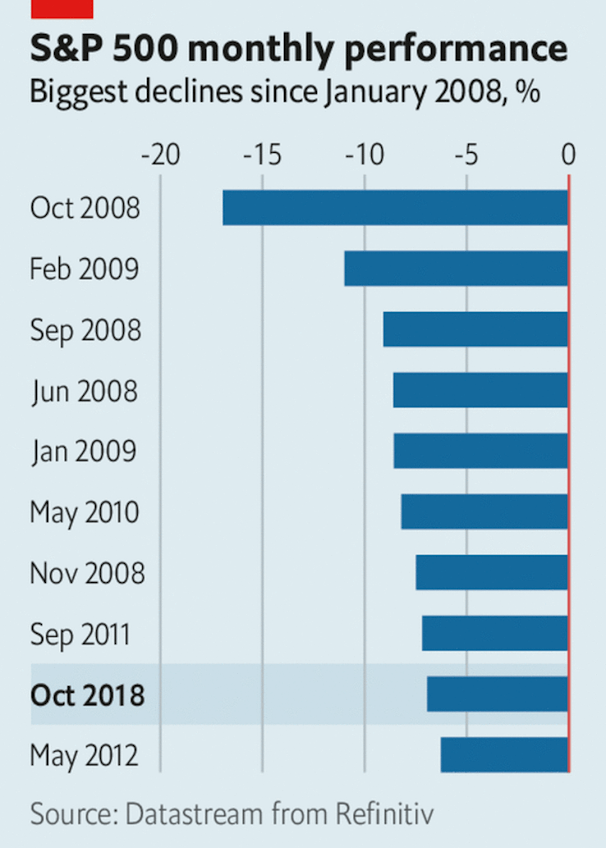

October saw the biggest market drops since my monthly portfolio tracking began in January 2013. In fact The Economist says October saw one of the top 10 biggest monthly falls in the S&P 500 since the 08/09 crisis.

The Sunday Times shows the worst months for FTSE since the 1960; October 18 isn’t one of the worst 10 but most of the worst ones were more than 30 years ago!

What was clear, as October drew on, was that everything seemed to be falling. Asian markets have had a tough year already, largely due to Trump trade spats. European equities have similarly faced trade headwinds. But now the USA, Oz etc fell sharply too. The Sunday Times has a nice graph in fact:

Most noticeable for some of us was the big drop in tech stocks. Some FAANGs had fallen 20% at points; only AAPL seemed relatively immune from the sharp change in sentiment.

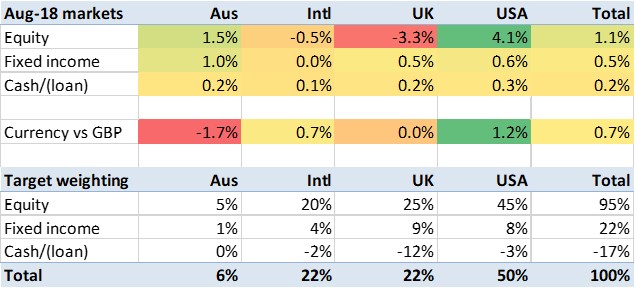

Amidst the hysteria, you’d have been hard pushed to notice that bonds were relatively unaffected by this carnage. UK corporate bonds actually went up almost half a percent. For once, correlations didn’t all converge.

Currency movements deserve a brief mention too. For UK investors October was another month of big Brexit-driven swings. The pound rose against the USD above £1:$1.32 at one point, before falling to £1:$1.27 where it pretty much finished the month. The dollar won the October currency battle, which took the edge off the S&P being the biggest casualty in the equity contest.