I’m not really sure what happened in August.

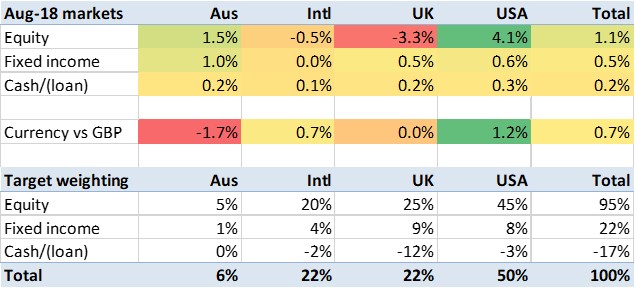

At least, you’d think something quite significant happened, given that UK equity markets fell over 3% and US markets rose over 4%.

The swing of the US:UK currency itself was notable during the month but over the month fairly minor – with the USD gaining slightly based on 1 August (but the gain having been much bigger only a week ago).

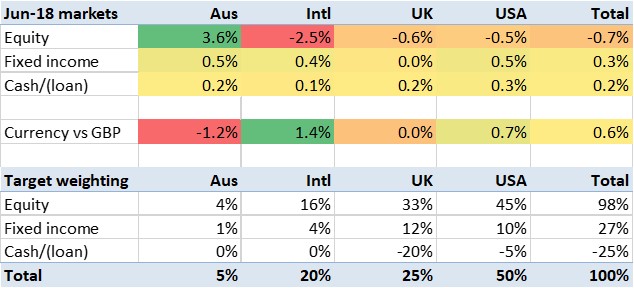

The Australians have joined the Brits, Americans, French, Italians and Swedes in bewilderment at the nonsense their politicians can get up to. But the Australian markets haven’t moved much; the currency fell and the equities rose in compensation.

The USA appears to be making more ‘progress’ on trade, with the news at the end of the month being about some Mexico/NAFTA-related agreement. Maybe that helped. Maybe.

In the UK we saw the media running with the ‘no deal’ ball. How much of this was silly season, and how much reflected the overlooked aspect of the Cabinet’s Chequers deal in which they agreed to take ‘no deal’ planning much more seriously, I couldn’t say. It has certainly nudged me to move my portfolio a bit more out of the UK than I might have done.

So, all in all whatever drove the big market movements in August somewhat passed me by. But 6 point swings between UK and US equity markets, after currency effects, are not common. Thank goodness I have almost double the allocation to the USA – which rose by over 4% – than to the UK – which fell by almost as much.