I am about a week late writing this monthly update, and my what a week it’s been.

February was when the coronavirus (now called covid-19) began to impact the markets. My diary called it the ‘corona correction’. At the time of writing, on the 10th March, the February story already seems rather old, but here it goes in extreme brevity.

- Beginning of February. I sold my house, pocketing over £1m cash.

- Middle of February: I ‘slowly’ dripfed £1m cash into the market, matching my target allocation.

- End of February: the market fell almost 10%. Doh.

- (early March – my house money has all gone…. but that’s getting ahead of myself!)

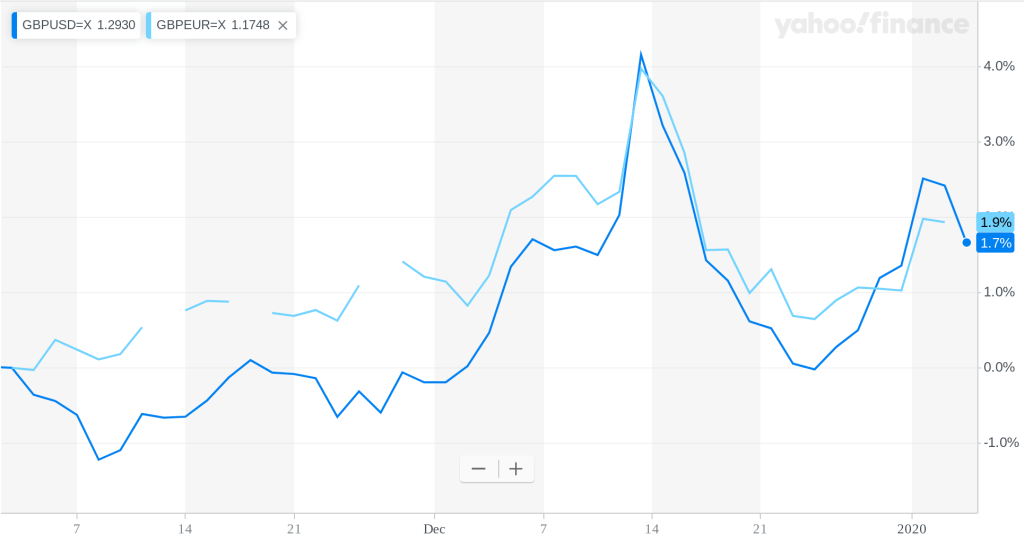

More specifically, equities fell 6-9% on the month (and significantly more off the mid-month peaks). Bonds ticked upwards very slightly. And the pound fell slightly versus other major currencies.

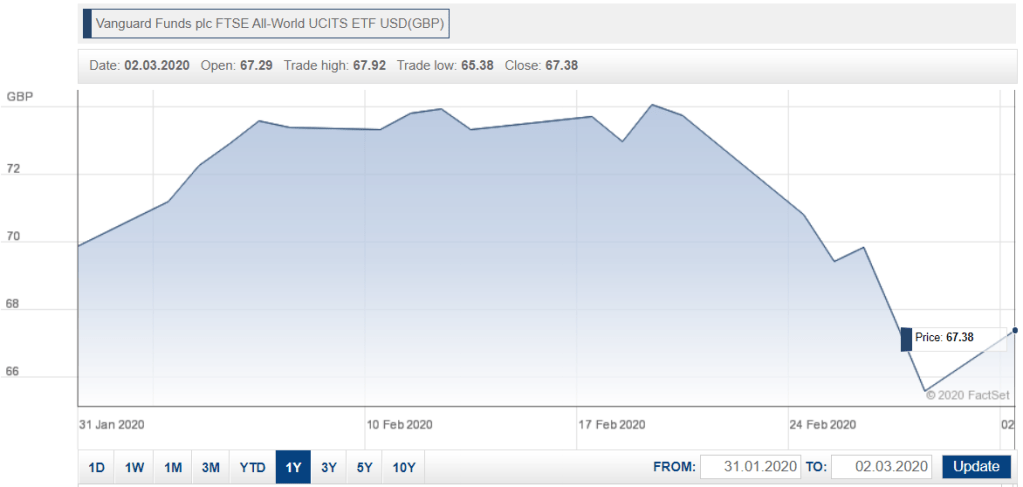

The markets, weighted to my allocation, fell 5.8%. My (very slightly leveraged) portfolio fell 6.4%, even more than the market – reflecting me topping it up by >£1m mid month, at its peaks. That high plateau you see in the graph below almost exactly mirrors the time period over which I put my money to work. Sigh.

The other thing February was notable for was my efforts to reduce my (taxable) complexity. I sold a number of holdings, in unsheltered accounts, replacing them with fewer, larger, mostly ETF holdings. And in my sheltered accounts (pension & ISAs), I sold a bunch of ETFs and bought individual securities – concentrating my active holdings in the (undisclosable) tax sheltered accounts, and reducing my number of (disclosable) tax holdings significantly.

My efforts fighting complexity were more successful, more quickly, than I would have first thought. I have reduced my total holdings to <150. My unwrapped (disclosable) holdings are almost below 100 – a reduction of 37 since the start of the year. And my number of small (<£20k) holdings has dropped to 35 (though the market’s falls are making this target harder to hit!).

My portfolio is still complex (certainly too much so for @mathmo – see comment below), but progress is being made – and quickly.

I liked FireVLondon’s revelation on the road to Shipley Tax Office that complexity was a real cost like fees and taxes. I myself just a few weeks ago pinged my tax return off with just 10 lines of information to my accountant so his inventory of tax filing effort was eye-opening. I’d suggest the solution didn’t go nearly far enough in the face of active naughtiness — if the cost of complexity were properly measured, the knife would have cut much deeper.

(@mathmo comment about my Fighting Complexity blog, in Monevator’s Weekend Reading 14 Feb 2020)

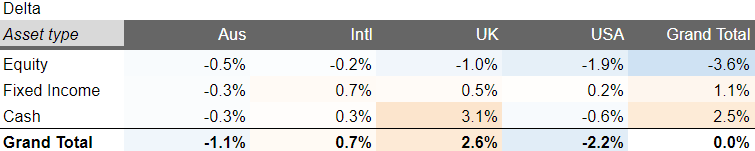

At the end of February, I was almost 4% underweight equities, around 1% overweight in bonds, and 2.5% overweight cash. With hindsight, not terrible positioning for the March roller corona-ster.