The UK election already seems some time ago. Really, it was just last month, and mid month too. And it provided welcome clarity – I will say that for it – after several years of frustration. For all the hyperventilating Brexit nonsense, citing ‘enemies of the people’, ‘a treasonous Speaker’, parliament undermining democracy etc, the root cause of much of the last few years’ nonsense was the lack of a majority in Parliament. Parliamentary sovereignty is supreme, and is delegated to the government/executive by a clear majority. All else is noise.

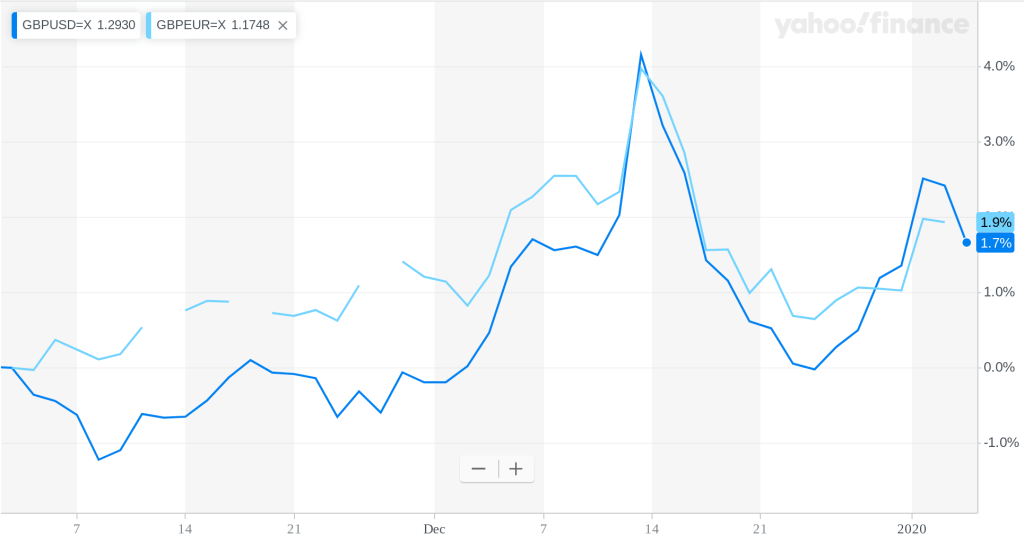

And much as I am no fan of the Tories and the Tory Brexit, the improvement in mood / confidence / sense of clouds lifting after the election result was palpable. The dimwit forex markets lifted the pound above $1.35, before dumping it back where it started once they came to their senses. By the end of the month though sterling had climbed 1-2% against the USD/EUR.

Elsewhere, we saw the new EU commission take over, the USA/China trade war rumble on, and some nasty early season bush fires take root in Australia.

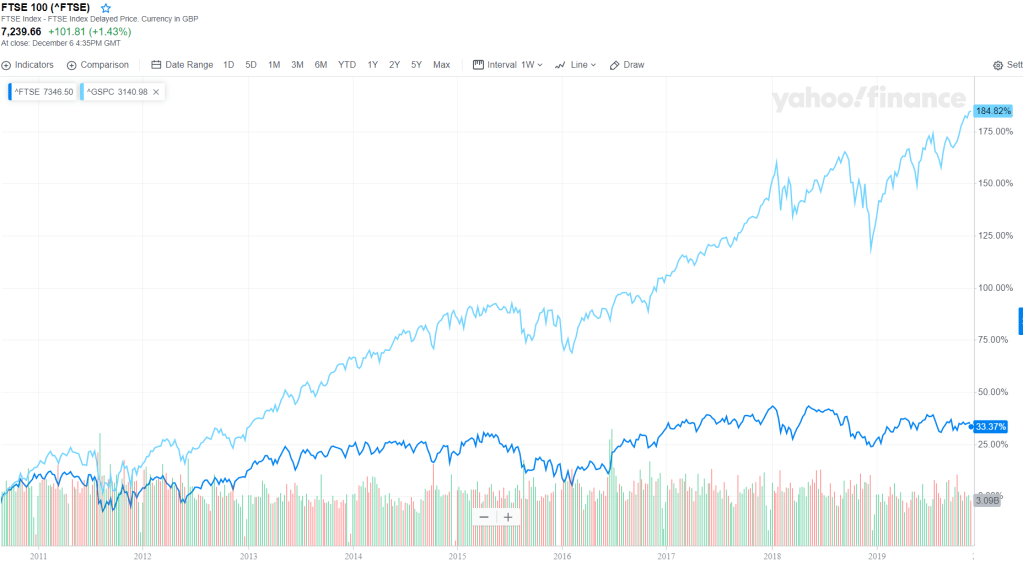

And amidst all this noise, equity markets rose. The UK market grew the fastest, bouyed by the election result presumably; both European and USA markets also saw good gains, admittedly mostly cancelled out by their currencies falling against the pound. Only Australia was the outlier, with a drop in its ‘share market’ somewhat mitigated by the rise in the AUD.

Continue reading “December returns and 2019 review”