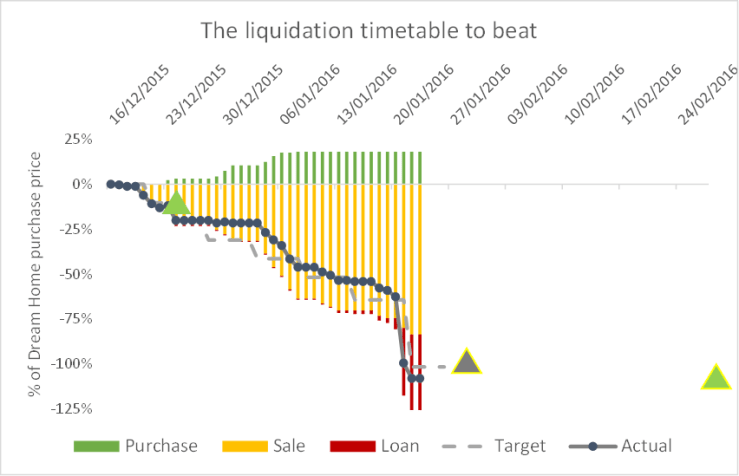

I’m nearing the end of my Dream Home purchasing odyssey. In fact I have mustered the cash needed to buy the home, and wired it to my lawyer, in good time for completion. Hooray!

What I haven’t quite found yet is the cash for the stamp duty, but I have another month to find that and think the market volatility could help. In any case you can see in my graph below that I have obtained over 100% of the purchase price – I am only a few % away from where I need to be including transaction fees etc.

This means that right now I am the proud owner of over £1m of new debt.